There are a number of programs widely available to prepare economic evaluations for

proposed investments. These programs typically use either simple payback and/or

discounted cash flow analysis. Unfortunately, these programs have often been

developed by governmental agencies or universities, which are not subject to income

taxes. As a result, they may ignore the impact of income taxes, which can influence

the outcome of economic analyses significantly. The discussion below illustrates the

effect of including income tax consequences in various forms of economic analysis.

Simple Payback

Using simple payback, the capital cost of a project is divided by the first year’s

expected savings to give an indication of how many years the project would take to

“pay back.” Economic analysts have railed against the use of simple payback for a

variety of reasons: it ignores the time value of money, it gives no credit for benefits

occurring after the payback period, etc. However, an equally damning aspect is

seldom mentioned: the fact that simple payback omits the effect of income taxes.

As a simple example, assume a proposed investment having the following

characteristics:

proposed investments. These programs typically use either simple payback and/or

discounted cash flow analysis. Unfortunately, these programs have often been

developed by governmental agencies or universities, which are not subject to income

taxes. As a result, they may ignore the impact of income taxes, which can influence

the outcome of economic analyses significantly. The discussion below illustrates the

effect of including income tax consequences in various forms of economic analysis.

Simple Payback

Using simple payback, the capital cost of a project is divided by the first year’s

expected savings to give an indication of how many years the project would take to

“pay back.” Economic analysts have railed against the use of simple payback for a

variety of reasons: it ignores the time value of money, it gives no credit for benefits

occurring after the payback period, etc. However, an equally damning aspect is

seldom mentioned: the fact that simple payback omits the effect of income taxes.

As a simple example, assume a proposed investment having the following

characteristics:

Tax Adjusted

Tax Life Payback Period

Five-year 5.1

15-year 6.4

39-year 7.2

Tax Life Payback Period

Five-year 5.1

15-year 6.4

39-year 7.2

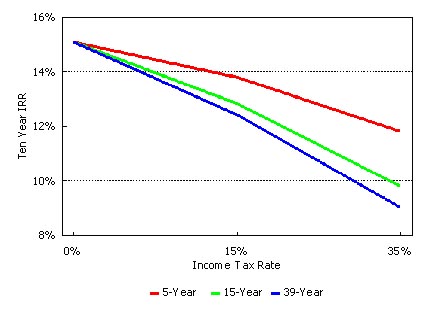

| Graph 1: Impact of Depreciation Schedule and Tax Rate on IRR |

Graph 1 shows how the expected return on an investment declines at higher tax rates

and longer depreciation schedules. If the proposal in question were for new HVAC

equipment to be purchased by an investor in a 35 percent marginal tax bracket, the

actual projected return on investment would be about nine percent. This is

substantially less than the 15-percent return projected when income taxes are

ignored.

The full impact of income taxes is probably best illustrated using net present value.

Using the same assumptions as above, and further assuming a ten-year study and a ten

percent discount rate, the results illustrated in Graph 2 were obtained.

and longer depreciation schedules. If the proposal in question were for new HVAC

equipment to be purchased by an investor in a 35 percent marginal tax bracket, the

actual projected return on investment would be about nine percent. This is

substantially less than the 15-percent return projected when income taxes are

ignored.

The full impact of income taxes is probably best illustrated using net present value.

Using the same assumptions as above, and further assuming a ten-year study and a ten

percent discount rate, the results illustrated in Graph 2 were obtained.

| Graph 2: Impact of Depreciation Schedule and Tax Rate on NPV |

In this example, a project that appears to have positive economics when ignoring

income taxes may actually have a negative NPV when income taxes are properly

accounted for. In other words, by ignoring income tax consequences, an investor

could actually make an inappropriate investment decision.

In preparing NPV analysis, a few cautionary words about discount rate are in order.

First, it is important that if after tax cash flows are to be discounted, an after tax

discount rate must be used. Otherwise, an invalid NPV will result.

Secondly, the cost of borrowing money is probably not the appropriate discount rate,

even though this has been used in countless analyses. Because a company’s ability to

raise capital funds is limited, companies invest in a portfolio of projects based on the

expected returns and relatives risks of these projects. Projects must compete with

each other to be included in the portfolio of acceptable investments. Therefore,

when evaluating a proposal, the appropriate discount rate is the return that the

company would expect on a competing investment having similar risk. Tax treatment

for competing proposals may influence both their expected returns and perceived

risk.

[One final note: projects currently being planned and for which equipment has been

purchased after September 10, 2001, and which will be placed in service before

January, 2005, are allowed special tax treatment].

income taxes may actually have a negative NPV when income taxes are properly

accounted for. In other words, by ignoring income tax consequences, an investor

could actually make an inappropriate investment decision.

In preparing NPV analysis, a few cautionary words about discount rate are in order.

First, it is important that if after tax cash flows are to be discounted, an after tax

discount rate must be used. Otherwise, an invalid NPV will result.

Secondly, the cost of borrowing money is probably not the appropriate discount rate,

even though this has been used in countless analyses. Because a company’s ability to

raise capital funds is limited, companies invest in a portfolio of projects based on the

expected returns and relatives risks of these projects. Projects must compete with

each other to be included in the portfolio of acceptable investments. Therefore,

when evaluating a proposal, the appropriate discount rate is the return that the

company would expect on a competing investment having similar risk. Tax treatment

for competing proposals may influence both their expected returns and perceived

risk.

[One final note: projects currently being planned and for which equipment has been

purchased after September 10, 2001, and which will be placed in service before

January, 2005, are allowed special tax treatment].

Investment $1,000,000

Electric savings $400,000

O&M Expenses $75,000

Fuel expenses $125,000

Net annual savings $200,000

Electric savings $400,000

O&M Expenses $75,000

Fuel expenses $125,000

Net annual savings $200,000

Calculating the simple payback as it is normally done:

| $1,000,000 ----------------- = 5.0 years $200,000 |

This calculation has two significant problems. First, it does not reduce the net

savings of $200,000 for the income taxes which must be paid. Secondly, it treats

the investment as though it were simply another expense, which could be written off

for tax purposes in the same year as the expenses for fuel and O&M.

In actuality, investments by tax-paying entities must be capitalized over a number of

years, adhering to schedules published by the IRS. The depreciation period varies

for different types of investments, referred to in the IRS Code as different kinds

of “property.” The depreciation period, or “tax life,” can vary from three to 39

years depending on: (1) what type of property is being depreciated, (2) how the

property is being used, and even (3) who owns the property.

To illustrate the complexity of selecting the correct tax life, consider that most

electric generating equipment is depreciated over a 15-year tax life, if it is not

owned by a public utility. However, if the electric generating equipment uses a

renewable fuel, such as hydro or biomass, the appropriate tax life is five years. A

condensing steam power plant owned by a public utility requires a 20 year tax life.

As another example, a chiller used in an industrial process can usually be depreciated

over a period dictated by the manufacturing process in which it is used -- usually

seven to ten years. On the other hand, a chiller used for space conditioning in an

office building would be depreciated over the same time frame as the building itself,

39 years.

The applicable tax rate may also not be obvious. It is important to use the investor’s

marginal tax rate for each new proposal. Any new project involves additional income

taxes, assuming it performs as expected and increases profits. Because these profits

are in addition to existing profits, the marginal, not average, tax rate should be used

for analysis.

Assuming a 35 income tax rate, (which would be close to what many companies pay,

including both Federal and state income taxes), the income tax adjusted payback

periods would increase from 5.0 years as follows:

savings of $200,000 for the income taxes which must be paid. Secondly, it treats

the investment as though it were simply another expense, which could be written off

for tax purposes in the same year as the expenses for fuel and O&M.

In actuality, investments by tax-paying entities must be capitalized over a number of

years, adhering to schedules published by the IRS. The depreciation period varies

for different types of investments, referred to in the IRS Code as different kinds

of “property.” The depreciation period, or “tax life,” can vary from three to 39

years depending on: (1) what type of property is being depreciated, (2) how the

property is being used, and even (3) who owns the property.

To illustrate the complexity of selecting the correct tax life, consider that most

electric generating equipment is depreciated over a 15-year tax life, if it is not

owned by a public utility. However, if the electric generating equipment uses a

renewable fuel, such as hydro or biomass, the appropriate tax life is five years. A

condensing steam power plant owned by a public utility requires a 20 year tax life.

As another example, a chiller used in an industrial process can usually be depreciated

over a period dictated by the manufacturing process in which it is used -- usually

seven to ten years. On the other hand, a chiller used for space conditioning in an

office building would be depreciated over the same time frame as the building itself,

39 years.

The applicable tax rate may also not be obvious. It is important to use the investor’s

marginal tax rate for each new proposal. Any new project involves additional income

taxes, assuming it performs as expected and increases profits. Because these profits

are in addition to existing profits, the marginal, not average, tax rate should be used

for analysis.

Assuming a 35 income tax rate, (which would be close to what many companies pay,

including both Federal and state income taxes), the income tax adjusted payback

periods would increase from 5.0 years as follows:

It is clear from this table that income taxes can influence an investment’s projected

payback period significantly.

Discounted Cash Flow Analysis

Simple payback is typically used only as a quick screening tool to eliminate projects

which are clearly not worth pursuing further. Discounted cash flow analysis uses

more sophisticated indicators, such as internal rate of return (IRR) and net present

value (NPV). In determining these indicators of economic viability, tax consequences

are also critical.

Graph 1 illustrates the impact of different income tax rates and depreciation

schedules. Again using the assumptions noted above -- a $1,000,000 investment and

a $200,000 net annual savings -- we further assume that there is no inflation in

savings or expenses.

payback period significantly.

Discounted Cash Flow Analysis

Simple payback is typically used only as a quick screening tool to eliminate projects

which are clearly not worth pursuing further. Discounted cash flow analysis uses

more sophisticated indicators, such as internal rate of return (IRR) and net present

value (NPV). In determining these indicators of economic viability, tax consequences

are also critical.

Graph 1 illustrates the impact of different income tax rates and depreciation

schedules. Again using the assumptions noted above -- a $1,000,000 investment and

a $200,000 net annual savings -- we further assume that there is no inflation in

savings or expenses.

| Economic Evaluation -- A Taxing Exercise |